Navigating rough financial waters can be daunting, but strategic debt relief efforts can provide a lifeline to stabilize your small business finances. Here are 8 essential moves to relieve debt pressures and chart a course to security.

Managing debt is a fundamental reality of running a small business. But when debts become unmanageable, it can feel like you’re trapped underwater with no escape. This comprehensive guide offers actionable strategies and expert insights to assist small business owners in navigating the complex world of debt relief. With the right approach, you can resurface your business finances and chart a course towards stability.

Assessing Your Small Business Debt Situation

Gaining clarity on your current debt levels is the critical first step. This involves thoroughly calculating total debts owed across all accounts and lenders. Categorize each debt based on key factors like:

- Interest rates – whether fixed or variable

- Payment terms – when payments are due, grace periods, balloon payments

- Collateralized vs unsecured – are assets or property tied to the debt?

- Amount owed – the total principal remaining

Additionally, examine the ratio of your business’s net income to recurring debt payments. If more than 50% of your revenue goes towards servicing debt every month, it signals an unsustainable situation that demands swift action. Debt loads exceeding 30% of income strain cash flow, while exceeding 50% makes it nearly impossible to cover operating expenses after accounting for debt payments.

Conducting a detailed cash flow analysis for your business also helps reveal how current debts impact day-to-day operations and your ability to cover essential expenses. Look at historical cash flow for the past 12 months. If debts constantly force you to miss payments to vendors or employees, or rely heavily on credit lines to finance operations, it diminishes the working capital available to sustainably run your business.

These assessments provide the comprehensive picture of current liabilities and their burdens required to strategize repayment. Don’t hesitate to involve financial experts like accountants to ensure you capture all relevant debts and fully understand the implications.

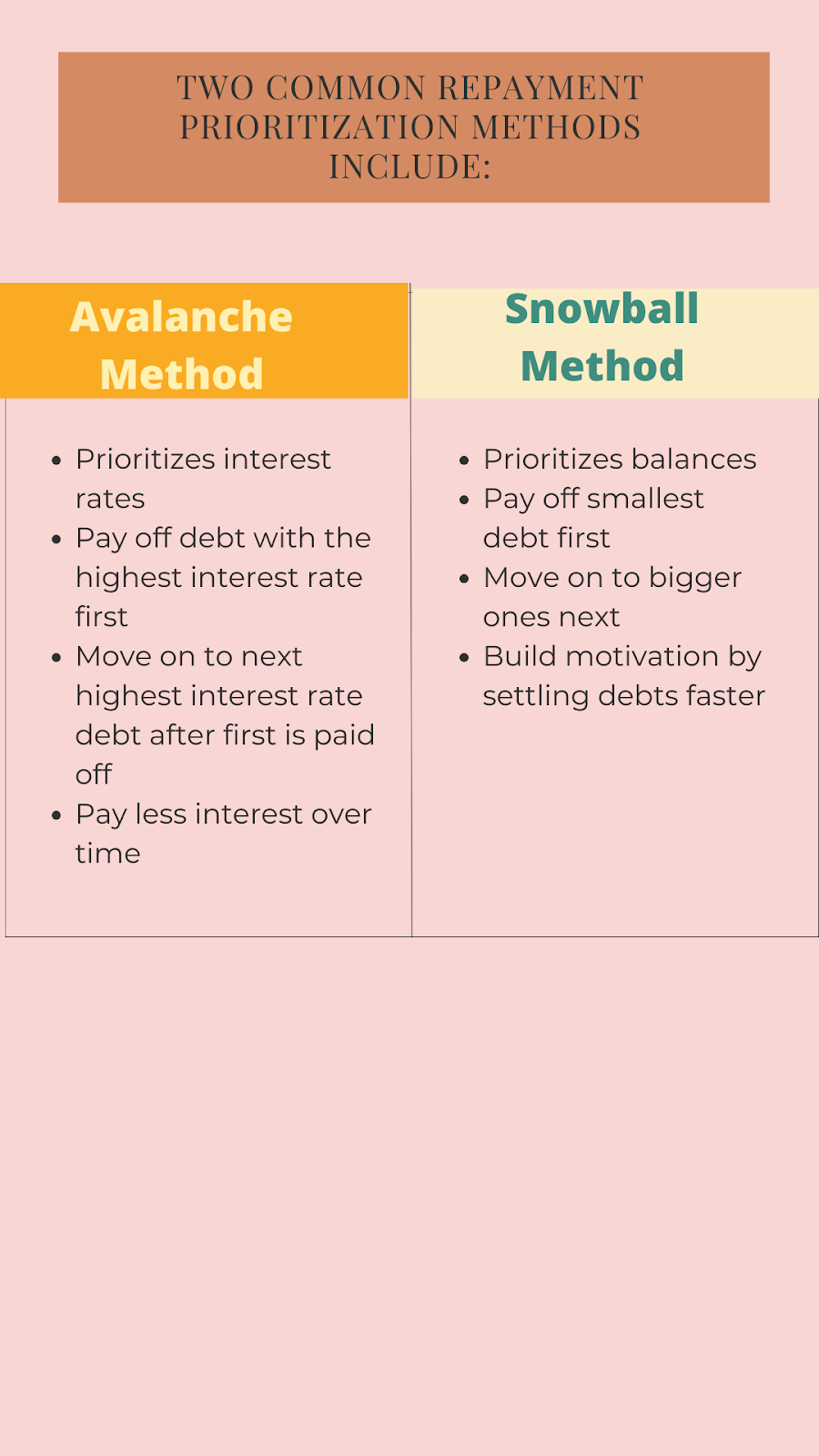

Prioritizing Debt Repayment Strategies

With all debts and obligations cataloged and their impacts quantified, the next step is strategically prioritizing which debts to tackle first.

Snowball Method: This method focuses on paying down the smallest debt balances first, regardless of interest rate terms. As you eliminate each small debt, you roll the payments that were going towards it into the next smallest balance. Like a snowball growing larger as it rolls downhill, this creates a snowball effect of accumulating payments which help pay off debts faster. Psychologically, the quick wins and growing momentum help maintain motivation.

Avalanche Method: With this approach, you prioritize paying down debts with the highest interest rates first, regardless of the balance amount. By eliminating your most expensive debt obligations, this method minimizes the total interest you pay over time. However, it may take longer to experience wins since high interest debts don’t necessarily align with the smallest balances.

For small businesses, hybrid approaches may work best to optimize both short-term motivation and long-term interest savings, ensuring a balanced approach. For example, you can allocate any extra income after making minimum payments towards attacking the highest interest unsecured debts first. This takes advantage of the psychology of quick wins from eliminating small balances, while also reducing expensive finance costs from high-interest unsecured debts.

Regardless of the exact method, thoughtfully ranking existing debts into a repayment priority roadmap based on your business’s specific situation is key. This transforms an overwhelming mountain of obligations into a step-by-step path forward. Revisit and re-evaluate priorities regularly as debts are paid down.

Exploring Debt Relief Options for Small Businesses

With repayment priorities set, investigating additional debt relief options can support the repayment process. Different forms of debt assistance can provide much-needed breathing room when business finances feel severely constrained.

Common debt relief options include:

Debt Consolidation

Pros: Simplifies multiple loan payments into one monthly payment, often at a lower interest rate, providing cash flow relief.

Cons: May require business assets as collateral for the consolidation loan. Also risks extending loan payoff timelines by spreading repayment over longer periods.

Negotiating with Creditors

Research negotiation techniques beforehand, maintain a cooperative tone, propose realistic payment plans based on ability to pay, and get any agreements for modified terms in writing before sending payments.

Debt Settlement

Involves negotiating with creditors to agree on a reduced lump-sum payoff amount as full settlement of what you owe. This saves money on total debt owed, but damages your business’s credit standing.

Nonprofit Debt Management Programs

Credit counseling programs that negotiate with creditors on your behalf to secure a centralized monthly payment, lower interest rates, and waived fees. This helps simplify payments but may extend loan terms. Different cities across the United States have varying levels of debt burden, with areas like New York, Los Angeles, and Houston often ranking among the highest for credit card debt.

Texas, in particular, has consistently ranked as one of the states with the highest credit card debt per capita in the nation. Finding the right debt relief option for Texas residents depends on their specific financial situation. Debt relief programs in Texas can help evaluate your circumstances and guide you through the process of negotiating with creditors, consolidating payments, and developing a personalized debt management plan tailored to your needs. When exploring debt relief programs, it’s crucial to verify that the organization is properly licensed and registered to operate in the state.

The right option depends on your business’s specific situation, debts, and financial goals. Weigh the pros and cons of each carefully, as some options like debt settlement or bankruptcy significantly impact creditworthiness.

Government and Non-Profit Programs for Debt Assistance

In addition to the above options, federal, state, and nonprofit programs also exist specifically to aid small business debt relief. Government agencies recognize the importance of helping viable small businesses overcome temporary setbacks to continue creating jobs and fueling local economies.

These programs include:

SBA Disaster Loans – Low interest loans up to $2 million for businesses severely impacted by natural disasters or declared emergencies. More flexible criteria than traditional bank loans.

Nonprofit Microloans – Small short-term loans distributed by community organizations to provide quick financing and targeted coaching to small businesses. Often more flexible than traditional bank financing.

State Small Business Credit Initiative (SSBCI) – State programs using federal funding to expand access to credit and financial assistance. Offers tools like loan guarantees, reserve funds for lending, venture capital financing etc.

Small Business Development Centers (SBDC) – SBA program providing management guidance and training including assistance with financial management and specifically debt restructuring.

SCORE Business Mentors – Nonprofit network of volunteer business mentors offering free counseling on strategies like financial management, business planning, and debt reduction.

Researching programs specific to your state and local community can uncover powerful resources to support small businesses through cash flow challenges. While not direct loans, this assistance provides much-needed breathing room when finances feel constrained.

Refinancing and Restructuring Existing Business Debt

For businesses with existing debt obligations like business loans or lines of credit, refinancing or restructuring current agreements can offer heavily burdened borrowers some debt relief options before resorting to consolidation or bankruptcy. Potential strategies include:

- Lowering interest rates – Especially beneficial for variable rate loans in high rate environments. This directly reduces monthly costs.

- Extending repayment timeline – Increasing length of the loan term reduces individual payment amounts, though total interest paid increases over the life of the loan.

- Modifying payment amounts – Maintaining the same repayment timeline but reducing periodic payment amounts provides immediate cash flow relief.

These adjustments provide cash flow relief by reducing near-term monthly repayment burdens, creating more breathing room for struggling businesses to improve their financial situation enough to meet original obligations. It also avoids taking on new consolidation loans that pile on fees and collateral requirements.

However, some key considerations apply when restructuring debt agreements:

- Check for any prepayment penalties on existing loans before trying to refinance. Triggering prepayment fees can negate potential savings.

- Beware excessively extending original loan durations. While this temporarily reduces cash flow pressure, it results in more interest paid over the life of the loan.

The key is finding the optimal balance between securing immediate financial relief through lower payments, while minimizing long-term costs by limiting repayment timeline extensions. Consult expert advisors to strategically restructure terms tailored to your situation.

Leveraging Assets and Business Equity

If restructuring and refinancing existing debt proves insufficient, more aggressive approaches like leveraging assets or equity can provide alternative avenues for securing funds to reduce debts.

Asset Liquidation

- Review business assets like equipment, property, inventory, or intellectual property. Identify opportunities to sell non-essential assets that are not pledged as existing loan collateral already.

- The influx of capital from sales provides funds to pay down high interest debts. However, carefully weigh short-term financial gain against potential loss of future revenue if assets sold prove difficult to re-purchase later.

Equity Financing

- Selling partial ownership stakes through equity crowdfunding platforms or taking direct investment in exchange for company equity helps raise capital quickly.

- However, giving up any business equity or control requires very careful evaluation of investor agreements. Seek expert legal guidance before finalizing any equity financing arrangements.

When prudently leveraging select assets or equity, these avenues create valuable capital influxes to pay down burdensome debts without taking on additional costly loan interest. However, the permanent loss of equity control or assets is a major consideration, so pursue options strategically aligned with your long-term vision.

Bankruptcy: A Last Resort Option

If debts remain persistently unmanageable despite exhausting relief options, refinancing opportunities, and asset liquidation, declaring bankruptcy may become the only viable path forward. While a difficult decision, bankruptcy provides a structured legal process to discharge debts and either liquidate assets or attempt to rebuild and restructure with a clean slate.

Chapter 11 Bankruptcy

- Businesses reorganize finances and repayment plans under court supervision. Leadership typically stays on to manage day-to-day operations.

- The restructuring plan involves converting debt into equity, selling assets to raise funds for creditors, or reducing/extending repayment timelines.

- Successfully emerging from Chapter 11 allows the business to continue operating without the burden of old debts they cannot repay.

Chapter 7 Bankruptcy

- All eligible business assets are completely liquidated and the proceeds distributed to creditors.

- Owners surrender control, as the court appoints a trustee to oversee liquidation.

- Any remaining debt after liquidating assets is discharged, but the business must cease operations.

Bankruptcy severely damages business credit standing for multiple years. Declaring bankruptcy should only be pursued as an absolute last resort after assessing all other options with legal advisors. With proper planning, many businesses do successfully emerge from Chapter 11 and Chapter 7 processes to rebuild and avoid repeating past financial management mistakes.

Maintaining Post-Relief Financial Health

For small business owners who navigate the rough waters of debt relief successfully, escaping the crushing debt burden offers a second chance to correct course and implement financial best practices to avoid spiraling back into distress. Proactive measures include:

Ongoing cash flow monitoring – Prepare detailed cash flow forecasts. Monitor projected versus actual expenses vigilantly to quickly catch variances.

Building operating reserves – Gradually build cash reserves to 3-6 months of average operating expenses to cushion against future income disruptions.

Conservative budgeting – Take an ultra-lean approach to variable operating costs like inventory and marketing expenses. Focus on profitability.

Profit-first mindset – Rather than incurring expenses then hoping enough sales cover costs, make strategic decisions to maximize profitability as the first priority.

With this combination of vigilant planning, budgeting, and cash flow controls, small businesses can avoid repeating past debt missteps. Numerous online tools and templates exist to implement these financial health practices, like the cash flow planner on QuickBooks or profit/loss templates on Finmark.

Frequently Asked Questions

What first steps should I take when realizing my small business has unsustainable debt?

First, thoroughly document all current debts and obligations. Then assess their full individual and collective impact on your finances using ratios like debt-to-income and tools like cash flow statements. These quantifiable insights allow you to gauge the severity of the situation and identify priority areas for addressing strained cash flow.

How do I decide between debt consolidation versus debt settlement for my business?

The choice depends on your goals. Debt consolidation is better for protecting credit score and business reputation, and simplifying payments long-term through refinancing. Debt settlement maximizes immediate debt reduction, but damages creditworthiness. Weigh options with advisors to determine the best path aligned to your objectives.

What are the pros and cons of Chapter 11 versus Chapter 7 bankruptcy for a small business?

Chapter 11 allows ongoing operations under court supervision, while Chapter 7 requires asset liquidation and closing the business. Chapter 11 preserves ownership control but involves a complex restructuring process. Chapter 7 offers a fresh start but at the cost of losing the business entirely. Weigh these tradeoffs closely with legal counsel.

What are the first steps to rebuild my business finances following bankruptcy?

After discharging unpayable debts through bankruptcy, focus on cash flow forecasting, building operating reserves, and taking a lean and profit-focused approach to managing finances. Be conservative with spending and maintain diligent financial oversight. Stabilizing cash flow and profitability provides the foundation to rebuild credit.

Are there any debt relief options specifically tailored for small businesses impacted by the COVID-19 pandemic?

Yes. The SBA offers targeted low interest Economic Injury Disaster Loans up to $2 million for COVID-19 impacts. The SBA Debt Relief Program also covers principal, interest and fee payments on existing SBA loans. Nonprofits also offer microloans to aid small businesses facing COVID-19 financial challenges.

Should I use the “snowball” or “avalanche” method to pay down my business debts?

The snowball method which pays smallest balances first helps build momentum through small wins, while the avalanche method focusing on highest interest rates minimizes total interest costs most effectively. Consider a hybrid approach targeting small high-interest debts first to optimize both psychology and finances.

How do I know it’s time to seriously consider bankruptcy for my small business debts?

Bankruptcy should be a last resort when you’ve exhausted all other options but debts still exceed sustainable levels, significantly constraining cash flow and threatening business viability. Consult experts to fully understand the legal implications. With proper planning, many businesses successfully rebuild post-bankruptcy.

What are some common mistakes small business owners make in debt management?

Inadequate cash flow planning and monitoring, overspending on discretionary expenses, failing to separate business and personal finances, improper use of credit, and not involving financial experts early enough. Addressing debt proactively is key.

Where can I find reputable credit counseling services to help my small business tackle overwhelming debts?

The National Foundation for Credit Counseling provides certified financial counselor referrals. They offer confidential debt management guidance and help negotiating with creditors. Reputable nonprofits like GreenPath also provide customized debt repayment plans.

How do I avoid spiraling back into debt problems after getting debt relief for my small business?

After debt relief, implementing strong budgeting, cash flow forecasting, profitability analysis, and operating reserves are essential financial best practices. Also leverage technology like online bookkeeping software with financial dashboards to maintain visibility. Conservative spending and diligent planning prevent repeat debt crises.

In Conclusion

While the road through debt relief is long and challenging, with dedication and commitment to financial wellness, small businesses can emerge stronger and better equipped to build lasting success.